Medical bills in my mind are some of the most stressful bills to get in the mail. It can be daunting when a medical bill arrives in the mail. I’ve written up steps you should take when you get a medical bill. When I get a medical bill thoughts that came to my mind include:

- Is it correct?

- Do I pay it or does my insurance?

- Am I responsible for the whole amount?

- Can I negotiate it down?

- Has my insurance already paid this?

- Can I ask my insurance to pay me back?

- What questions do you have?

Open it!

Always open it immediately and see what it is.

Don’t ever ignore it! The sooner you open it the sooner you can do something about it.

Look carefully at it and don’t pay it immediately

I know it may sound crazy to say open it and NOT pay it immediately, I want you to look at the charges very carefully and make sure it is correct before you pay it.

The two key points are:

- Are the charges accurate?

- Did you have the services that were listed?

If the bill is not detailed enough call the hospital or doctor’s office and ask for a detailed bill. They should be able to provide you with one. Did you actually have knee surgery? How many teeth did you have filled? (Hint: This one may be tricky to determine)

“Accounts of medical billing errors vary widely. While the American Medical Association estimated that 7.1 percent of paid claims in 2013 contained an error, a 2014 NerdWallet study found mistakes in 49 percent of Medicare claims. Groups that review bills on patients’ behalf, including Medical Billing Advocates of America and CoPatient, put the error rate closer to 75 or 80 percent.” NBCNews Business article

Go to your insurance’s website to look at your Benefits

It is so important to understand what your benefits cover.

- Do you have a deductible? The amount you need to fully pay before your benefits start. In some cases, you will have to pay 0%-25% (called co-insurance) after you have reached your deductible. Make sure you understand how much you will need to pay. Sometimes your company’s HR paperwork will be more clear about deductibles and co-insurance.

- What is your family’s out of pocket max? This is how much you have to spend during the year before your insurance will cover the rest at 100%. Look closely at what your insurance counts toward your deductible. You want to make sure everything that you do spend is included in that deductible. This can include prescriptions, labwork, doctors visits, specialists, and co-pays.

On your insurance’s website, get a copy of the Explanation of Benefits (EOB)

Your EOB is not a bill. It is information about what your insurance covers. Always take a look at it and confirm if the doctor’s office or hospital charged you correctly and your insurance company is covering the costs that they are responsible for.

Each insurance company has a different layout for their EOB and also timing for their EOBs. If the one you receive is confusing, give them or your HR office a call. Insurance reps are happy to go over the EOBs with you. They want to make sure you understand them.

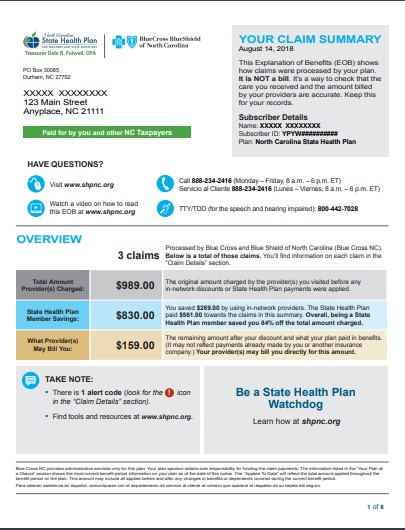

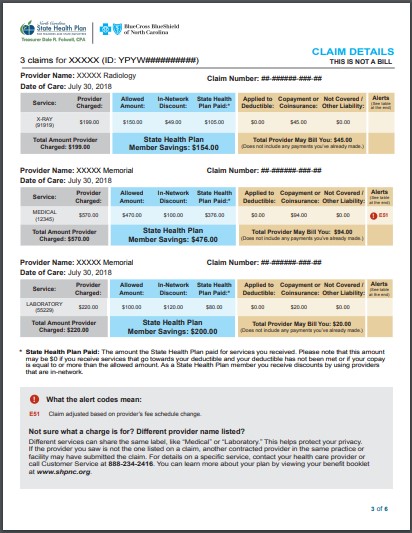

Here is an example of Blue Cross Blueshield EOB.

It includes the date of service, the provider charged, allowed amount, and what is applied to deductible.

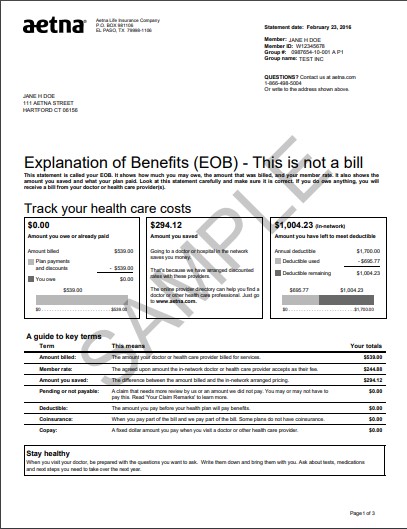

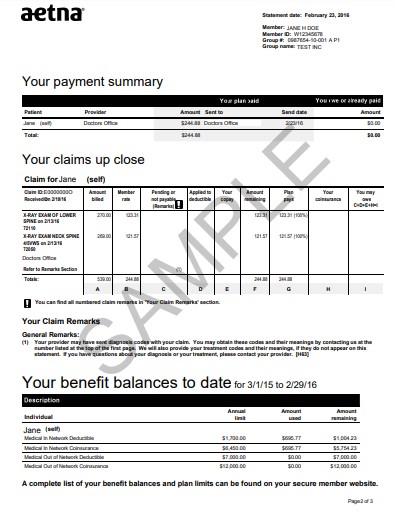

Here is an example of Aetna EOB which also includes service date, the provider charges and what is covered.

If there isn’t an EOB that matches your medical bill, this is a red flag! Did the doctor’s office actually submit a claim to your insurance?

In some cases, the doctor’s office hasn’t submitted the claim, or they have the incorrect insurance information. Call the doctor’s office and find out if they submitted a claim to the correct insurance. If they have incorrect insurance information you also want to confirm this as soon as possible. If they didn’t submit a claim or submitted it to the incorrect insurance company make sure they get that correct information and resubmit it. In most cases, it will go through in the next week or so and everything will match up to a new EOB.

Does the medical bill and EOB match?

This is key. You want to make sure that the amount they are requesting matches. If your doctor’s visit says $126.00 make sure the insurance EOB also says $126.00. If it doesn’t match you can call the doctor’s office to get a corrected claim submitted to the insurance company. Otherwise you may be responsible for the difference see below for more information about balance billing.

Is the medical bill a “balance bill”? This means that the insurance company already paid the doctor’s office and the doctor’s office is asking you to pay the remainder balance.

This is very important to look at carefully because this isn’t allowed for in-network providers. The providers have already negotiated with the insurance to only charge an approved amount.

If you think you were sent a balance bill, you should see what the EOB says you actually owe. If it doesn’t match this is a good time to call your doctor and point out what the EOB says.

Another thing to check is: are the codes correct?

This is where you need to talk to your doctor’s office to make sure they are filing the correct codes for the visit. Each procedure has a specific code. If they have filed for the wrong code your insurance may not cover it. You can ask the doctor’s office to resubmit the claim with a different code.

If you call the provider and they don’t want to work with you what do you do?

Above issues with billing you need your provider to help you. In most cases, they want to help you and will be happy to resubmit claims to the insurance and correct codes. If they are not being helpful, the next step is to talk to your insurance company. They have negotiated rates with the in-network provider and should be able to help and provide guidance on what to do next.

What if the medical provider is out of network?

This is handled differently than an in-network provider. Like above you want to make sure the provider submitted a claim to your correct insurance. If everything above is correct, the correct insurance, date, amounts and the insurance says the provider is out of network and will only cover a certain amount.

Did you have a choice of providers? If you were in a hospital or medical facility and had no choice of the provider then the insurance company should provide coverage.

“Some state laws also step in to protect insured consumers from charges they incur for out-of-network emergency services during a hospital visit (i.e. you picked an in-network hospital, but the surgeon or anesthesiologist isn’t in network).” NBCnews Business article

They should treat the provider as an in-network provider. This is where it is best to talk to your insurance company and state the following:

“I had no choice of this provider and needed this service. Please resubmit this claim.”

This tells the insurance company that you had no choice. Then call the out of network provider and state:

“I called my insurance company and they resubmitted my claim. Since you are an out of network provider, could you please accept the insurance payment my insurance provides?”

In most cases, the answer is yes. If not, then talk to them to find out what you can do to reduce the final bill. They maybe able to do payment plans, 0% interest rate for a period of 6 months or more.

Pay your Bill

As long as the EOB and medical bill are correct and they follow your insurance plan, you are now required to pay your bill. You want to pay your bill in a timely manner. Thanks to technology you can pay your bill online for most billing offices which have safe ways to pay using a credit card, or debt card. If the doctor’s office only accepts checks as payments, you can use your bill pay feature at your bank and have them send a check. In some cases, some hospitals and doctor’s offices are offering 0% payment plans to make it easier to pay it off and some are offering 6 months or more.

If you don’t pay your bill the changes of it going to collections is high and this can affect your credit score.

In fact, the Consumer Financial Protection Bureau reports that around 31.6% of adults in the United States have collections accounts on their credit reports. That’s almost one in three Americans! Medical bills account for over half of all collections with an identifiable creditor. Chances are good that you too have a medical bill in collections. Credit.com Medical Bill Myths

If you are having financial difficulties, it is always best to be up front and say you are:

“I can’t pay that amount right now, I can only do this amount ____. “

Hospitals and doctor’s offices want to get paid just like all businesses and they don’t have a lot of time and energy to hold onto bills for long periods of time which is why doctor’s bills do go to collections faster than people think. Even if you do arrange a payment plan or adjustment to any bill make sure you get it in writing so you have proof of the changes.

Always monitor your credit reports on a regular basis using the free credit reports you get for free each year, most banks and credit cards are offering free monitoring as well as other free services.

Don’t forget your FSA or HSA

In open enrollment with your company you can sign up for a FSA which is called a Flexible Spending Account or HSA called a Health Savings Account if you have a High Deductible Plan. The FSA is an account where you put in pre-tax money in from your paycheck. This is a great way to save on taxes. Beware! You have to use it or lose it. Thanks to new rules by the federal government some companies will allow you to roll over up to $500 into the next fiscal year. To be on the safe side estimate what you think your bills will be. You can learn about qualified expenses and how to use your FSA by talking to your HR and looking here for more guidance.

Note: The rules have changed this spring 2020 so you can make mid-year changes to your FSA. Here is the article here.

The HSA is called a Health Savings Account connected with a High Deductible Plan. This account is awesome! The reason is it is an account that you can keep forever. You also have the option to keep the money in cash or invest the money in index funds or mutual funds by your HSA investment account company. The best part is the money is taken out of your paycheck pre-tax and will grow tax free and you can take the money out for qualified medical expenses at anytime tax free. You just need to keep those receipts and EOBs mentioned above. More details about an HSA can be found here.

So remember you can use these for any qualifying expense. This is a great way to save as well. Let me know if you have any questions.

Contact me if you need some support to figure out how to handle some of this. Also let me know if you have any questions or concerns.

In closing, I hope this article helps you better understand how medical billing works.

FraidyCat Finance says:

What to do if you don't have an Emergency Fund? - Microstuff says:

Jessica Medina says: